💼 [NEW GUIDANCE] VAT DECLARATION & PAYMENT FOR EXPORT PROCESSING ENTERPRISES (EPEs)

Export Processing Enterprises (EPEs) often wonder:

Do we have to declare Value-Added Tax (VAT)? And in which cases?

The Hung Yen Tax Department has provided clear and official guidance as follows:

✅ 1. When EPEs are NOT required to declare VAT

- ✔ EPEs are NOT required to declare or pay VAT for processing/manufacturing activities for export.

👉 These are considered non-tariff zone activities, and therefore not subject to VAT declaration.

✅ 2. When EPEs MUST declare and pay VAT

EPEs must declare VAT when they engage in any business activities outside the scope of export processing.

Examples include:

- • Purchasing goods from the domestic market for export (right to export).

- • Importing goods and selling them into the domestic market (right to import).

- • Other commercial transactions not considered export processing activities.

📌 3. Conditions for VAT declaration on non-export activities

🔹 Separate accounting

EPEs must separately record:

- Goods – revenue – expenses for export processing activities

- Goods – revenue – expenses for non-export activities

🔹 Tax registration with the domestic tax authority

To declare VAT for non-export activities, EPEs must register for tax with the competent local tax office.

🔹 Separate storage areas

Storage areas for export-processing goods must be clearly separated from areas used for

other business activities (sales into the domestic market, import/export rights…).

📅 4. VAT declaration period

🔸 Monthly declaration

Under Point a, Clause 1, Article 8 of Decree 126/2020/ND-CP,

monthly VAT declaration is the default requirement for EPEs.

🔸 Quarterly declaration

If the EPE’s total revenue in the preceding year ≤ VND 50 billion,

it is eligible to declare VAT quarterly

(Point a, Clause 1, Article 9 of Decree 126/2020/ND-CP).

🧾 5. Invoice usage

- • Under the credit method → use VAT invoices.

- • Under the direct method → use sales invoices.

- • When selling into the domestic market or non-tariff zones, invoices must state:

👉 “For organizations and individuals in non-tariff zones.”

🎯 SUMMARY – EPEs DECLARE VAT ONLY WHEN:

- ✔ They conduct commercial activities beyond export processing.

- ✔ They perform separate accounting and have proper tax registration.

- ✔ They apply the correct monthly or quarterly declaration period.

- ✔ They use the correct invoice type according to their VAT method.

📩 Need MBA Audit to review your EPE vs. non-EPE model, separate accounting, or import–export–inventory documentation?

We are always ready to support your business. 💚

- 📌 Do Intern Students Have to Pay Social Insurance from July 1, 2025?

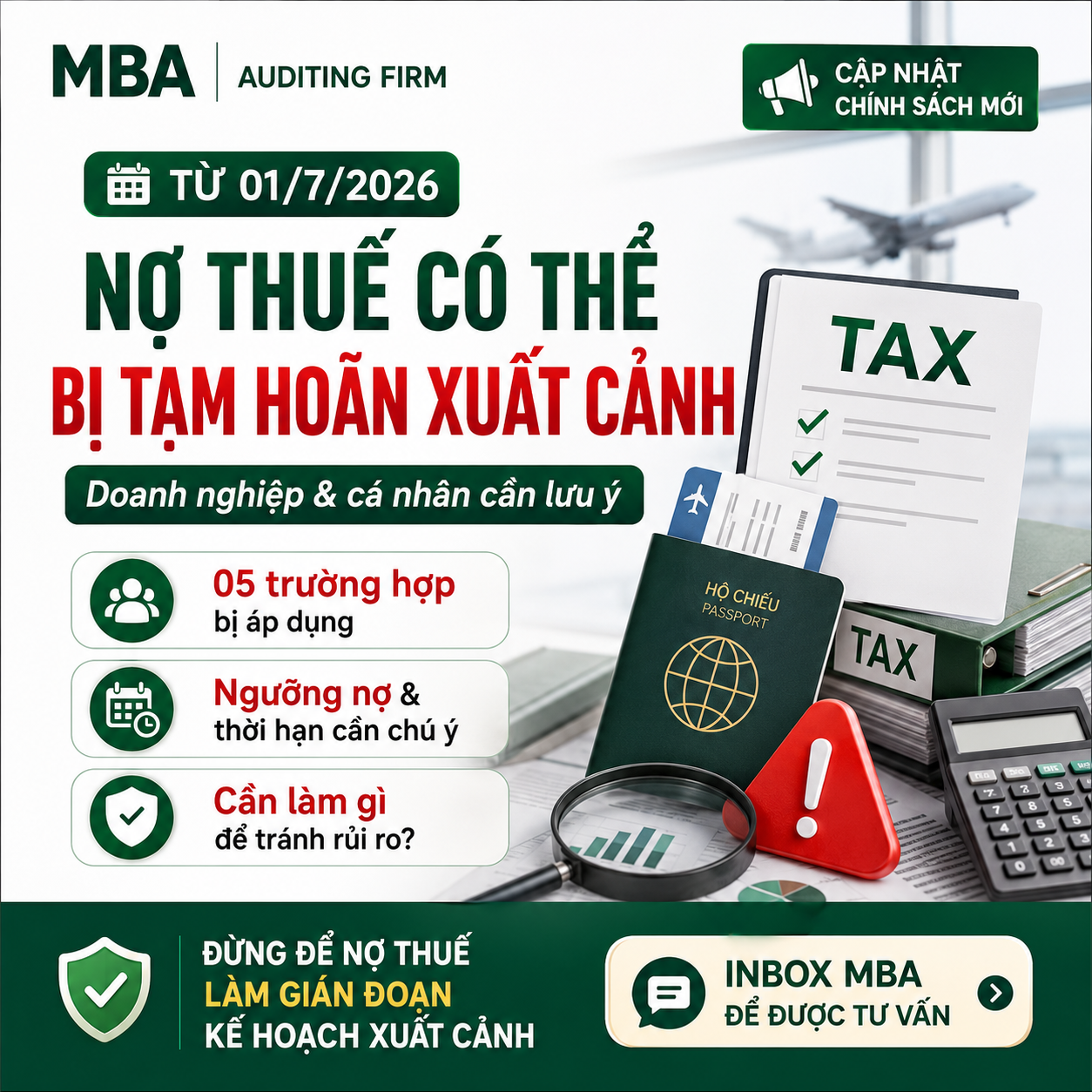

- 🚨 FROM 1 JULY 2026: OUTSTANDING TAX LIABILITIES MAY RESTRICT EXIT FROM VIETNAM

- 🚨 OFFICIAL UPDATE – Effective from 01/01/2026: Personal Deductions Increase to VND 15.5 Million/Month

- 📢 SUGAR-CONTAINING SOFT DRINKS: SUBJECT TO SPECIAL CONSUMPTION TAX → NOT ELIGIBLE FOR 8% VAT REDUCTION

- 📚 Collaboration Agreement Ceremony between Ho Chi Minh City Open University and MBA Auditing Firm Company Limited