🔍 ALL OVERTIME PAY WILL BE TAX-FREE FROM 2026 – RIGHT OR WRONG?

This is a question that many enterprises and employees are concerned about when

Law on Personal Income Tax 2025 officially issued.

👉 The answer is: RIGHT, but we still need to understand the true nature of the law.

✅ 1. From January 1, 2026, how is overtime pay exempt from personal income tax?

📌 Clause 8, Article 4 of the Law on Personal Income Tax 2025 specify the types of

income that are exempt from personal income tax, including:

Night shift pay, overtime pay; salaries and wages paid for days not taken as legally mandated leave.

📌 Article 29 of the Law on Personal Income Tax 2025 provides:

- The Law takes effect from July 1, 2026;

-

However, provisions on income from salaries and wage

apply from the tax year 2026.

👉 Therefore, for enterprises applying the calendar year as the tax period:

✔️ All overtime pay for resident individuals is exempt from personal income tax

from January 01, 2026.

⚖️ 2. New points compared to the old regulations

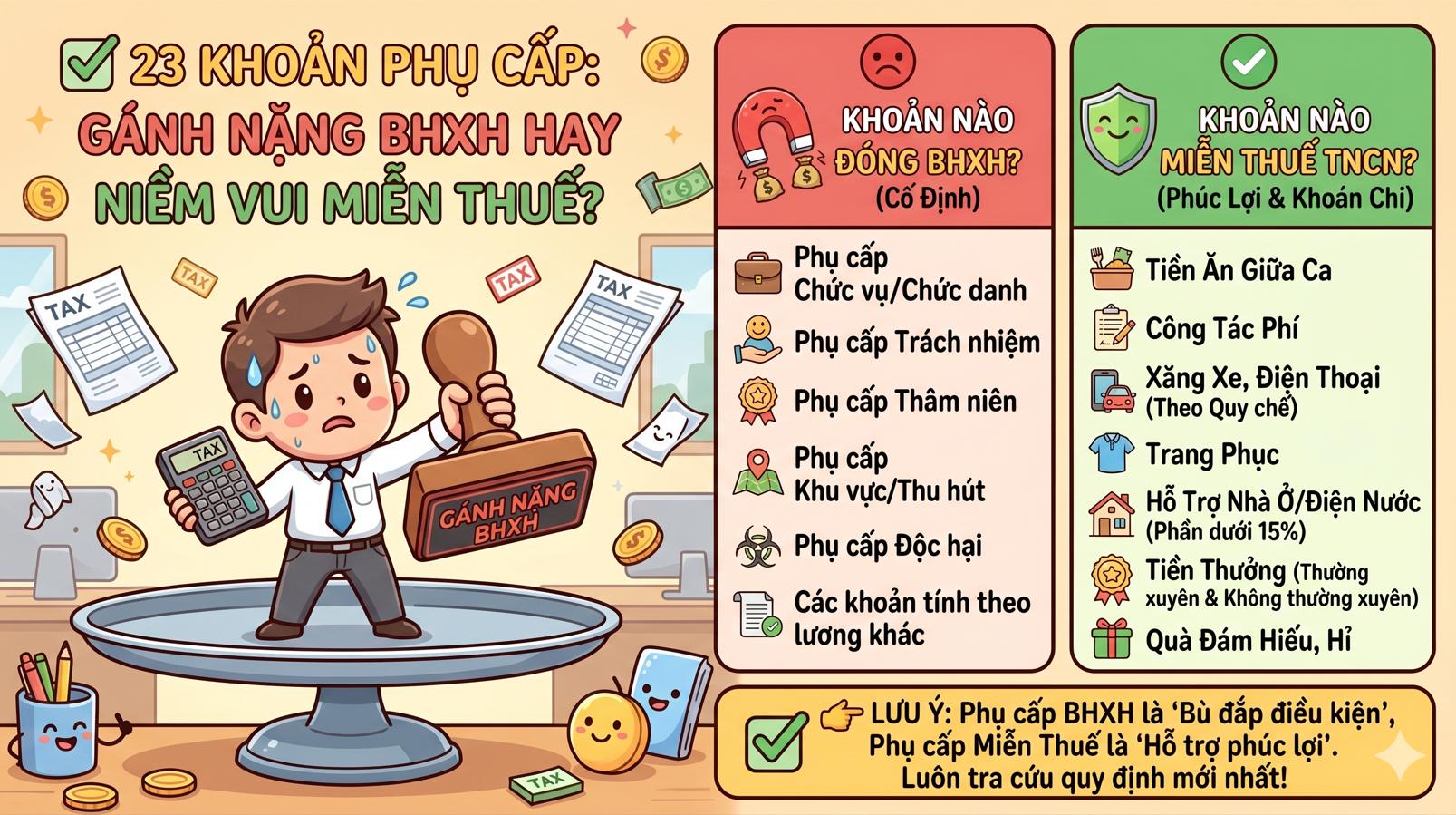

🔹 According to the Law on Personal Income Tax 2008 (Clause 9, Article 4):

👉 Only the portion of overtime pay that exceeds the normal working-hour wage is tax-exempt.

🔹 Under the Law on Personal Income Tax 2025:

👉 All overtime and night shift pay is exempt from personal income tax.

📌 This is a very important change that directly benefits employees.

📋 3. Income SUBJECT TO personal income tax from salaries and wages

(Based on Article 3 of the Law on Personal Income Tax 2025)

- Salaries, wages and other payments of a salary or wage nature.;

- Remuneration, monetary or non-monetary benefits;

-

Allowances, subsidies and other income, except for exempt income as stipulated

(Preferential allowances for meritorious individuals, national defense and security allowances,

social insurance benefits, severance pay, social welfare benefits, etc).

👉 Note: Overtime and night shift pay are exempt from tax under Article 4 ,

and therefore are not included in taxable income from 2026.

👤 4. Who is subject to personal income tax??

📌 Based on Artical 2 of the Law on Personal Income Tax 2025, Taxpayers include:

- Resident individuals with taxable income arising both within and outside Vietnam;

- Non-resident individuals with taxable income arising in Vietnam.

👉 A resident individual is a person:

- Who is present in Vietnam for 183 days or more in a year or within a 12-month period; or

- Who has a permanent residence in Vietnam.

🔎 CONCLUSION

✔️ From the 2026 tax period (January 1,2026):

👉 All overtime and night shift pay received by resident individuals

is exempt from personal income tax.

✔️ Enterprises need to review their personal income tax calculation, payroll and

payroll software in order to apply the new regulations correctly.

📚 Legal basis: Law on Personal Income Tax 2025.

- 🔍 ALL OVERTIME PAY WILL BE TAX-FREE FROM 2026 – RIGHT OR WRONG?

- 🚨 OFFICIAL UPDATE – Effective from 01/01/2026: Personal Deductions Increase to VND 15.5 Million/Month

- 🚨 [HOT NEWS FROM 10/06/2025] #Business_Households are officially divided into 3 TAX GROUPS

- OFFICIAL: STARTING FROM THE 2025 CORPORATE INCOME TAX PERIOD, TAX PERIODS OF LESS THAN 3 MONTHS ARE NO LONGER ALLOWED TO BE COMBINED

- VAT Changes in Vietnam After July 1, 2025 – What Businesses Must Know