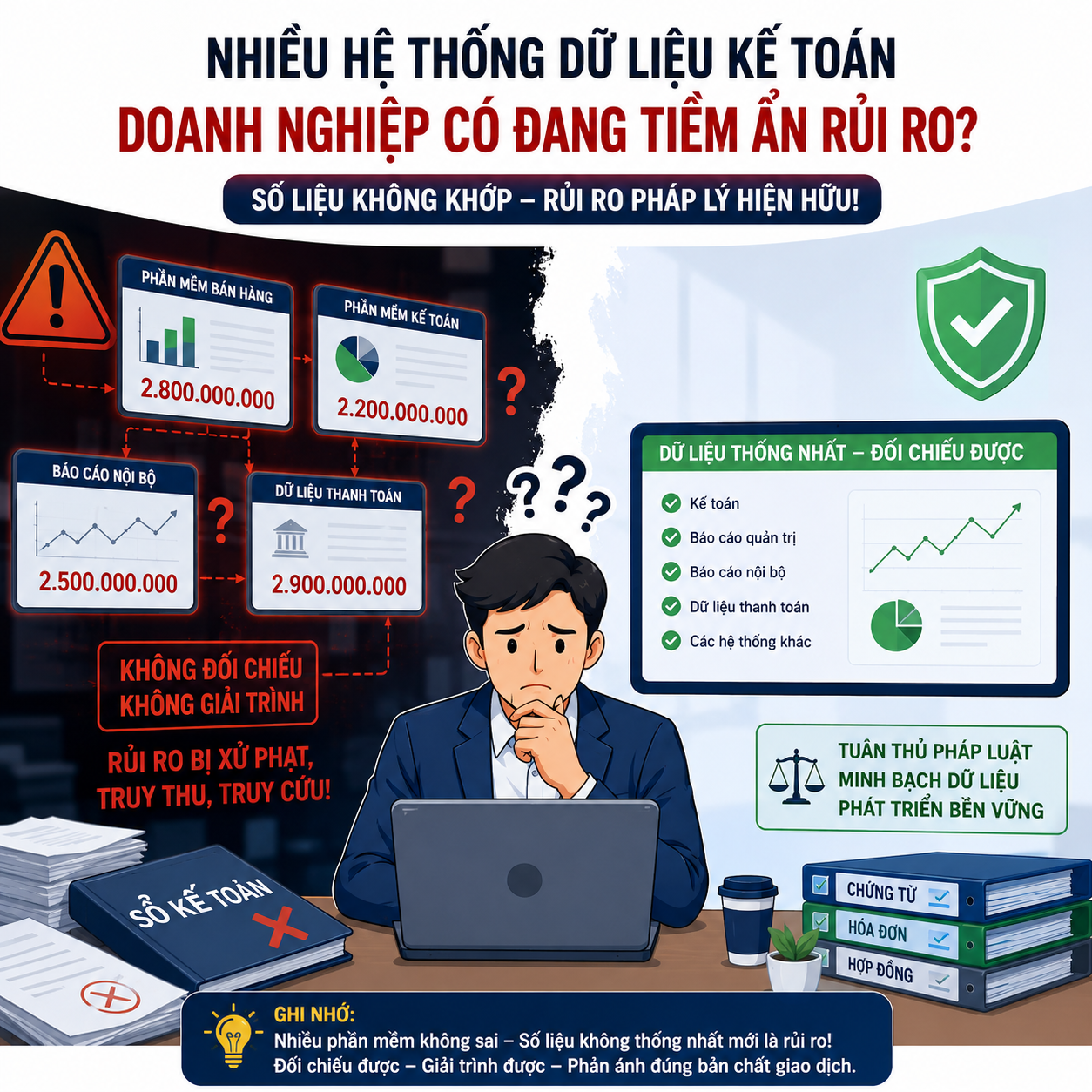

📢 OFFICIAL DOCUMENT 1902/CT-CĐS: TIGHTENING CONTROL OVER “TWO SETS OF ACCOUNTING BOOKS” – LAUNCHING A COMPREHENSIVE DATA REVIEW

This official document is not merely guidance… but a signal of a completely new phase in tax administration:

Data-driven management – Technology-based tracing – Elimination of “two sets of accounting books”.

📌 1. General Information

- No.: 1902/CT-CĐS

- Date: 31 March 2026

- Issuing Authority: Tax Department

- Target entities:

- Electronic invoice service providers

- Accounting software providers

- Electronic transaction service providers

🎯 Objective: To prevent tax fraud through the use of two sets of accounting books.

🚨 2. Nature of the targeted conduct

Enterprises use:

- One set of accounting books for reporting to the tax authorities

- Another internal set of books to record actual revenue

👉 Purpose:

- to reduce tax payable

- to conceal revenue

📌 The tax authorities consider this to be systematic fraud supported by software and technology.

⚖️ 3. Legal basis – Very high risk

- Law on Accounting 2015 – Article13: Prohibits maintaining two sets of accounting books

- Law on Tax Administration 2019:

- Article 17: Tax declarations must be truthful and complete

- Article 143: Failure to record revenue may constitute tax evasion

- Criminal Code 2015 – Article 221:

- Maintaining two sets of accounting books may result in criminal liability

🔥 4. The Tax Department’s position

All economic transactions must be fully – accurately – promptly recorded in a single accounting system.

- “Two sets of books” → cause loss of state budget revenue

- Undermine fair competition

- Erode trust in the legal system

🧠 5. Tightened control measures (EXTREMELY IMPORTANT)

🔹 (1) Prohibition of “two-set” accounting software

Suppliers must not develop or integrate functions hat enable the operation of two accounting systems.

🔹 (2) Installation of warning mechanisms

- Log data changes

- Detect abnormalities

- Issue warnings on fraudulent conduct

🔹 (3) Real-time data connectivity

- Integrate sales, accounting and e-invoicing data

- Transmit data to the tax authorities on a transaction-by-transaction basis

🔹 (4) Reporting suspicious enterprises

- Suppliers must report enterprises showing signs of using two accounting systems

- The information must include: the enterprise’s name, tax identification number and address

🔹 (5) Submission of customer lists

⏰ Deadline: The full customer list must be submitted no later than 8 April 2026

Thereafter, monthly periodic reports must be submitted

📊 6. Appendix – Comprehensive Data Collection

- Customer name

- Tax code

- Software Used

- Period of use

- Status (New/Amended/Discontinued)

👉 This is the step toward building a nationwide database on enterprise accounting software systems.

🚨 7. Understanding the true nature

This is not a ordinary official document , but a signal of:

- Data-driven tax control

- Technology-based tracing

- The complete elimination of “two sets of accounting books”

⚠️ 8. Practical impact

For enterprises:

- There is no longer any room to “circumvent” controls through software

- Data will be cross-checked

- The risk of inspections will increase significantly

For accountants:

- It’s no longer possible to maintain two sets of accounting books as before

- Data must be synchronized across sales, invoices and accounting records

📌 9. Conclusion

👉 Three keywords of this official document:

Transparency – Connectivity – Traceability

💥 Clear message:

Any enterprise still using “two sets of accounting books” → will be discovered sooner or later

- 📌 Do Intern Students Have to Pay Social Insurance from July 1, 2025?

- 📢 NEW OFFICIAL LETTER – GUIDANCE ON THE PERSONAL INCOME TAX SCHEDULE APPLICABLE FROM 2026

- 👉 VAT REFUND CONDITIONS FOR EXPORTS – DON’T GET IT WRONG!

- INDIVIDUALS RENTING HOUSES – BUSINESSES NEED TO PAY ATTENTION

- 🔔 UPDATE ON SOCIAL INSURANCE, HEALTH INSURANCE, AND UNEMPLOYMENT INSURANCE CONTRIBUTION RATES EFFECTIVE FROM JANUARY 1, 2026